What is process automation?

Process automation in the banking sector can be broadly summarised in two categories.

Intelligent process automation involves restructuring data that could not be adequately processed prior to process transformation due to poor organisation. An easy-to-understand example is opening a bank account in the shortest possible time. By using artificial intelligence, banks can make the structuring of data much easier and faster. AI takes the form of a chatbot or a simple upload of documents to the bank’s website, for example.

Traditional process automation, on the other hand, is limited to very straightforward processes, such as robotic process automation (RPA). This involves replacing manual processes in particular with mechanical rules, such as moving objects from A to B.

Automation opportunities in the banking sector

In order to optimise processes in the banking sector, decision-makers must ask themselves essential questions to determine whether and how much potential can be realised:

- Phase 1: Will I still need this process in the future?

- Phase 2: Can this process be standardised – and thus automated?

- Phase 3: Can I further simplify this process and omit individual steps?

- Phase 4: How can I speed up the process, make it more efficient or automate it?

In phase 4, the solution approach and thus the technical components that are suitable for optimisation or digital transformation are determined.

Which possible solutions can be implemented?

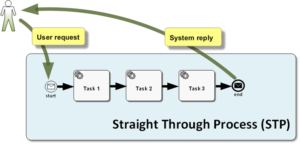

Option 1: Straight Through Processing (STP)

The partially heterogeneous, mature architecture is replaced by a stringent system. This solution enables or, in some cases, requires a complete overhaul. This has advantages, as there is no need to deal with numerous interfaces and old systems. However, it also involves enormous costs (including integration, migration, etc.).

Option 2: Business process management solutions (BPM)

Business process management (BPM) solutions are a similar approach, but one that is compatible with existing IT architecture. In other words, these are workflow solutions that can be integrated into the existing system landscape (front and back end) of banks and insurance companies as a middle layer, thereby enabling automated processes.

Option 3: Robotic process automation (RPA)

Robotic process automation (RPA) is a technology that uses software bots to automate individual process components, acting as a “band-aid” for unconnected processes. RPA bots are the third-best, but now widely used, method for process automation. They are fast and cost-effective, meaning they have a short payback period. Companies can use the technology to increase efficiency in specific cases in the short term.

What are the potential implications of the various approaches in the banking sector?

Option 1: Straight Through Processing (STP)

- Automated and accelerated payment procedures

- Standardisation of processes

- Automated e-commerce authentication

- Increased customer satisfaction through ease of use (customer happiness, brand loyalty)

Option 2: Business process management solutions (BPM)

- Transparency across processes and systems

- Central documentation of processes

- Improved quality of business processes

- Relief for employees through optimisation and automation of routine tasks

- Reduction in costs

Option 3: Robotic Process Automation (RPA)

- Increased process efficiency and customer satisfaction

- Increased capacity to handle transaction volume

- Focus of employees on important tasks

- New sources of revenue

- Increased customer loyalty

- Efficient product and service marketing

Our experience and projects already implemented

- Business Process Engine

A BMP solution was introduced at our customer’s site for a large number of approval processes. As part of our consulting activities in the credit and risk environment, we contributed to the design and implementation of the IT solution using BMP tools to identify beneficial owners in the credit approval process.

- Credit risk insurance software – preliminary analysis

For the complex and manual process of extending a credit agreement to include CRI, which was previously managed using manual to-do lists and Excel spreadsheets, we designed and evaluated a preliminary analysis of an STP solution. The solution included both the technical documentation of the individual process steps and interfaces to credit inventory systems and databases. This would enable the new solution to be used to import business types and maintain inventory data.